Back in 2011 when I first joined Launch Capital, we started a project to see if we could find untapped markets that would prove to be huge markets and produce huge wins but find them early enough so that we could get ahead of the wave and get our bet(s) in before everyone else figured it out.

While we are still working on ways to uncover untapped markets, one of the interesting things we have discovered is that when a startup appears heralding a new sector, it often is the only entrant for a long time, often for years. Then there is a trickle, and an exponential rise to flood.

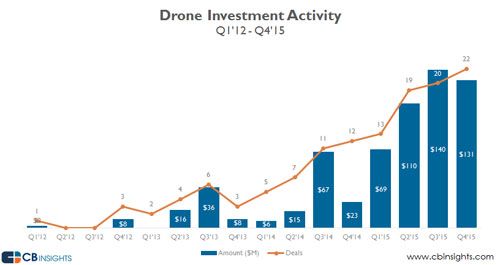

Take the Drone sector, for example. One analog for “hot-ness” of a sector is the amount of dollars investing into it. Here is a graph of Drone sector financing dollars from Q1 2012 to Q4 2015:

Source: CBInsights

Who was that lone drone startup who got funding back in Q1 2012? 3D Robotics, the very first funded drone company, co-founded by Chris Anderson, best selling author and WIRED editor. It was all about DIY back then. 3DR supplied UAV kits and seeded the first self built drones into the marketplace. Let’s call this the “First Contact Phase.” 3DR was around for a year before the next 3 were funded in Q4 2012. Let’s call this phase the “Trickle Phase” where a few more start appearing. It wasn’t until 2013 that a few more drone startups got funded, and then there was a lull until the 2nd half of 2014 when drones exploded into 2015. Let’s call this phase the “Flood Phase.”

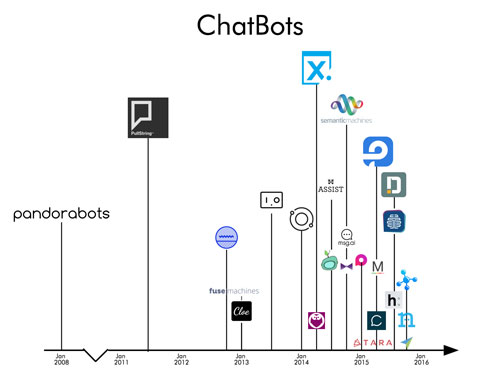

Here is a look at another sector: chatbots. We took a look at the chatbot industry and made a rough graph of startups across time (it’s a tough category because there are many working on bots, and many are working on it inside of other companies. We did our best pulling out those who are solely working on a chatbot):

The first startup appeared in 2008. Then things were very quiet for years until 2014, 6 years later, when things really started to take off. For startups, that is a long time to be surviving. It is possible that without industry and sector hype, there is suppressed availability for revenue and funding.

In either case, in the year before the main take off of the sector, there is a slow trickle of startups, and then it explodes.

When would be a good time to invest, for pre-seed/seed investors like us? Would it be better to invest in the First Contact Phase, or wait until the Trickle Phase happens? Or should we invest into the Flood Phase?

First Contact Phase

The most risky time to invest is when the first one that appears. You have the least evidence of a sector trend taking off at some time in the near future or happening at all.

For example, how would we know that drones or chatbots would take off instead of falling into obscurity or even death/dormancy until market conditions were more favorable? The first startup could try vainly to survive and die because they run out of money trying to create the market.

What drives an investment into a startup like this? It is through factors driven solely by belief. Belief in the entrepreneurs. Belief in shaky market factors that show little or no attraction to their products and services. Your own belief that this could be the next big thing. There is not much other evidence otherwise.

In theory, valuation would also be most favorable given lack of traction and sector trend evidence, although in recent years valuation variance at super early stage has not been all that much compared to others with traction and sector trend evidence.

Competition is non-existent by definition of being first, which does give this startup a unique opportunity to build the market without interference from any other companies.

Trickle Phase

A little bit less risky phase to invest in is investing in the Trickle Phase. You didn’t bet on the first, but now the second has appeared, maybe another few. Still the question remains – “Am I too early?” If you’re too early, some startups will die before the main wave appears; they didn’t raise enough money to survive long enough to catch the wave or were not able to get enough revenue.

In this phase, the market still questions whether these companies are viable and whether customers really want their products or not.

Valuation of these companies again may be lower than when the sector grows, but in today’s world, valuation may not differ much than in the First Contact Phase.

Competition increases as more startups enter the sector.

Flood Phase

And there is the Flood Phase: entrepreneurs, investors, customers, even media are all driving excitement and traction exponentially upward.

Sector trend factors are highest in evidence as many startups enter the field, and investors are putting a lot of money into them. Customers are trying out their products and services in hopes that they will gain the touted benefits.

Valuation marches upward as more conservative investors feel FOMO and must get in their bets on the trend or get left behind. Earlier startups who have managed to survive either First Contact or the Trickle Phase have gained traction and revenue, and later stage VCs invest in those, thus further motivating entrepreneurs to build companies in that sector because it is firmly hot. The media finally notices and posts are abundant about this new trend which adds even more fuel to the fire.

Competition is highest here as entrepreneurs build copycats to those who got funded before, and startups appear to tackle smaller segments of the sector. Investors who believe competition validates the market are validated!

Fast and Furious Acceleration into the Flood

As the title of this post suggests, it is amazing how fast a sector trend can move from Trickle to Flood. If you think about the overall sector I invest in, which is internet/mobile/software startups, it is easy to build something, too easy if you ask me.

When it becomes apparent that investors funding startups in a certain sector, other entrepreneurs also appear. In today’s world where accelerators are pumping out 100+ startups a year, and with the presence of media outlets who cover new startups, it is easy for someone to find a new sector to build something in, build it fast, and get out there for fund raising.

Investors are also self serving; they like to pump up the sectors they invest in for hopes that a Flood Phase will pick their own investments and drive them higher in value.

With software being so easy to write and with so many channels of public information, it basically takes nearly a year for a sector to enter and exit the Trickle Phase and explode into the Flood Phase. A year seems like a long time, but for investors it can take you by surprise. You see some hints, you process. You have conviction about some, you don’t about others. You make some bets, pass on others. If you’re an angel, you may be one of the ones saying “I love you but come back when you have a lead.” Now you’re waiting for other validation which can be slow in coming. By the time you get through all this, it’s already the Flood Phase.

Questions

The two essential questions to be answered for me are:

1. Which phase should we invest in?

I think that the phase you invest in is related to what kind of risk profile you have as investor (which makes sense) coupled with your belief and conviction about the startup and sector trend.

I’ve personally invested across all 3 phases. Of course, I’ve had more failures at the First Contact Phase where risk is highest. You make your bet and keep your fingers crossed. Looking back at my portfolio, the fastest growers have always been First Contact Phase investments.

My Trickle Phase startups have done well, depending on the circumstances.

I’ve made the least number of bets at the Flood Phase. I don’t like it when there is too much competition at the time of investment, especially at (pre-)seed. Valuation tends to be at the upper range which doesn’t work well with our fund economics.

For other investors, I think that later stage works best during the Flood Phase where it can be hard to pick the winner out of a large number of possibles, and it may be better just to wait for the winners to appear out of the noise. First Contact and Trickle Phases are better for investors who want to play in early stage.

The biggest accelerators are best positioned to see sector trends forming, as they see the most amount of startups through their applicants into their batch programs. They also see startups before the startup data companies do, because they only see startups AFTER a funding event happens. In addition, accelerators are often driving sector trends in the sense that they see something worthy of accepting and then media coverage of their demo days pushes new trends out to the public.

2. How do we find the next big sector trend?

This is the essential question that – well – can’t be answered for investors. Why? Because the answers are in the future! How can you predict the future? You can’t! HOWEVER, I think you can take some guesses and chances.

Whenever somebody appears working on something completely new, I look into it. If I never have heard of it before, I will immediately dive in. Unlike 99% of the other investors I’ve met, it is validating to me when THERE IS NO COMPETITION. If there is no competition, it is also possible that these guys are a First Contact startup in a new trend that hasn’t gotten too hot yet.

We’ve also spent a number of years looking into how to find the next big sector trend and, as you can imagine, it’s super hard looking for something that doesn’t exist. We are still trying!

Playing the market like an accelerator also helps; you must have enough conviction and resources to deploy investment broadly and be ok with a high error rate.

Many thanks to Julia Vlock for putting together the research for this post.

Finding the Next Big Thing: The Pace of Sector Growth is Fast and Furious

Leave a reply